Imagine that you recently celebrated your 40th birthday and finally decided to learn about the importance of saving for retirement. You may have even bought a book or magazine about it. Except, it says that you should have started saving for retirement in your 20s. You’re well past that age and still haven’t even started saving for retirement.

Fortunately, you do have options, even if you’re getting a late start.

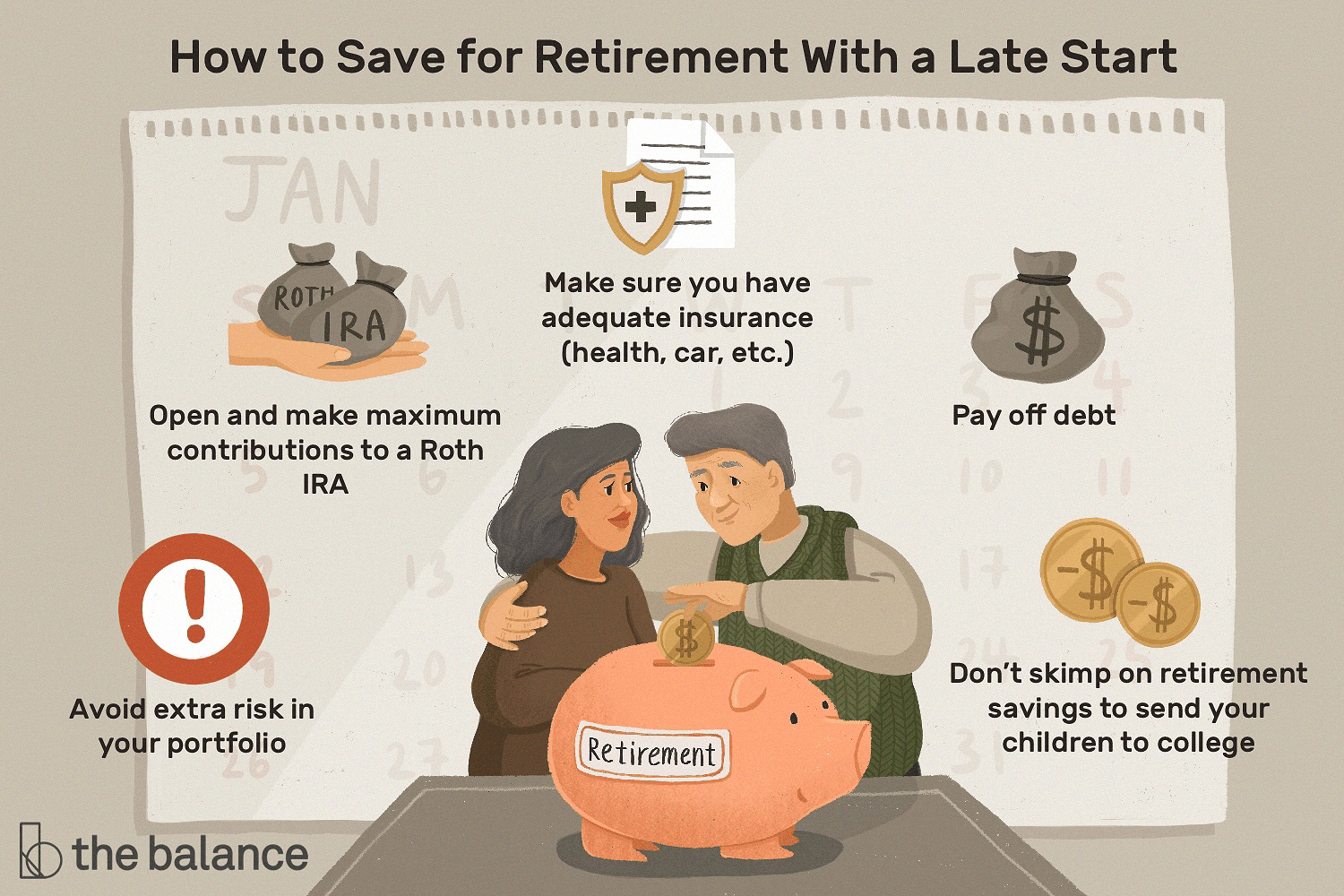

Key Takeaways

- Maximize your annual retirement savings.

- Set a reasonable dollar goal.

- Avoid unreasonable risk.

- Consider a Roth account.

- Make sure you have adequate insurance.

- Pay down high-interest debt.

- Don’t go broke to put your kids through college.

Play Catch-Up

Assume you’re 40 years old, with $0 in retirement savings. At your age, in 2021, you’re legally allowed to save $19,500 in a 401(k) retirement plan; After you turn 50, you’ll be able to contribute an additional $6,500 in catch-up contributions. Those are the maximums set by the Internal Revenue Service (IRS).

Note

In 2022, the contribution limit for 401(k) plans increases to $20,500, though the catch-up contribution amount remains the same at $6,500.

With a 7% rate of return, your 401(k) account balance could grow to $1 million in 22 years and 10 months if you contribute the maximum amount each year. You’d be on track to have more than $1 million by the age of 63.

As you can see, the magic of compounding makes it possible to achieve your retirement savings goals even if you start late.

Identify How Much Savings You Need

You might tell yourself that you don’t need a million dollars or that you just want a simple life. But even a simple life can require $1 million in the bank after you quit working. Most experts agree that you should withdraw no more than 3% to 4% of your retirement portfolio each year during your retirement. If you do the math, 3% of $1 million is $30,000, and 4% is $40,000.

In other words, if you want to live on an income of $30,000 to $40,000 per year in retirement, you’ll need a portfolio of at least $1 million. That assumes you won’t have a pension, rental properties, or other sources of retirement income. It also excludes Social Security income.

Don’t Take on More Risk

Some people make the mistake of taking on additional investment risk to make up for the lost time. The potential returns are higher: Rather than 7%, there’s a chance that your investments can grow by 10% or 12%.

But the risk, the potential for loss to your principal, is also much higher. Your risk should always be aligned with your age. People in their 20s can accept greater losses, since they have much more time in which to recover. People in their 40s can accept less risk, and people in their 50s still less.

Don’t accept extra risk in your portfolio. You might consider one of the following asset allocation formulas:

- Invest a percentage of 120 percent less your age in stock funds, with the rest going into bond funds. This represents a high but acceptable level of risk.

- Invest a percentage of 110, minus your age, in stock funds, with the rest in bond funds. This comes with a more moderate level of risk.

- Invest a percentage equivalent to your age in bond funds, with the rest going into stock funds. This is a more conservative level of risk.

Open a Roth IRA to Save More

Once you’re done maxing out your 401(k), open an IRA and maximize your contribution to that as well. A 40-year-old who is eligible to fully contribute to a Roth IRA can add considerable extra money each year to their retirement savings.

Contributions to a Roth IRA grow tax-free, and qualified withdrawals are tax-free. You’ll even avoid capital gains tax on the growth of your contributions.

Buy Adequate Insurance

Most personal bankruptcies are caused by an unexpected calamity. Reduce your risk by purchasing adequate health insurance, disability insurance, and car insurance. If you have dependents, consider term life insurance for the duration of time that your dependents will rely on you financially.

Many financial experts say that whole life insurance is generally not a good option, especially if you’re starting the policy in your 50s.

Look for planners who have a “fiduciary duty” to you as their client.

Note

Many financial experts say that whole life insurance is generally not a good option, especially if you’re starting the policy in your 50s.

Pay Down Debt

Try to pay off credit card debt, car loans, and other high-interest or non-mortgage debt since it can weigh you down financially. However, paying down your debt should not make you sacrifice your savings goals. It is important to have a financial plan to pay off your debt and save for retirement.

Also, consider whether you should make extra payments on your mortgage. If you’re in the early stages of your mortgage, and most of your payment is being applied toward interest, it might make sense to pay down some of that principal. If, however, you’re in the final years of your mortgage and your payments are primarily being applied to the principal, you may be better off investing that money for retirement.

You and Your Spouse Come First

Don’t waste your retirement savings plan to send your children to college. Your kids have more options and opportunities than you do. Your 401(k) may or may not allow you to take out a loan on your retirement account balance.

In any case, your children have their entire lives ahead of them. They can start saving for retirement in their 20s and 30s. If you’re in your 40s, you can’t turn back the clock and regain those decades of saving for retirement. Thus, the best gift you can give your children is your own financial retirement security.

Frequently Asked Questions (FAQs)

How do you start saving for retirement?

If you don’t have a 401(k), IRA, or any other retirement account, opening one of those should be your first step in saving for retirement. These accounts offer tax incentives that can enhance your savings. You can open a Roth IRA with a brokerage as easily as you can open a bank account. Simply provide basic personal information, link it to an existing bank account you have, and draw funds from that bank account to start saving. Once your retirement account is funded, you can put it into investments like stocks, bonds, or target-date mutual funds.

When does the average person start saving for retirement?

According to the Federal Reserve’s latest “Report on the Economic Well-Being of US Households,” 62% of Americans between the ages of 18 and 29 have some amount of retirement savings, but only 28% felt like their savings were “on track. ” This increases to 71% and 34%, respectively, for those between the ages of 30 and 44.